Some recent comments regarding college education costs in another thread made me wonder where the GRM brain trust fell on college costs and your responsibility, and what you think you should do for your kids. Where do you stand?

1) I believe the parents should foot the bill for all college and college related expenses for their kids.

2) I think parents should help, but no full ride. Maybe cover most of tuition (or community college), but they're on their own for room and board, but you can live in the basement for free.

3) Want to go to college? Do it yourself. When I was a kid we walked both ways up hill in the snow to work in a coal mine. Student loans exist for a reason. Get a job.

...or somewhere in between?

The average cost of an in-state four year public university tuition and fees in 2012 is just shy of $40K. (excluding books/housing/food/etc.) Projected Costs Data As of October 2012, the average amount of student loan debt for the Class of 2011 was $26,600, a 5 percent increase from approximately $25,350 in 2010. source

Public vs. Private tuition? Grad School? If your kid gets a scholarship do you reduce your assistance or still gift them what you had saved?

I've got 3 young kids, ages 8, 5, 5. I'm more inclined towards option 3, with some of option 2 thrown in.

My parents threw me out of the house when I was 19, I'll admit much of it was my own doing (they didn't help matters). I put myself through college. I went to several community colleges, then went to a state funded school. I took out loans for everything, and after I had been on my own for a few years I started getting a lot of grants. I also worked while going to school...a lot.

A few years after I was thrown out, I was on more speaking terms with my parents. They helped me some, but certainly didn't pay everything. Yes, I had student loans to repay when I was done and it sucked. But it also taught me a E36 M3 load about being responsible and making smart choices, financially and otherwise.

I intend to help our kids during college, but also expect them to do much/most of it themselves. College is expensive, but I see nothing wrong with starting at a community college and/or using a state school. If they do that and get loans, I'll certainly help them and make sure they don't get completely buried in debt before they graduate.

Depends on the college. If my daughter stays on her current trend of straight A's, she is headed to Dartmouth or Penn or Princeton or some such place. I will not be able to afford all of that! I will be paying a small percentage of her costs.

If she decides to stay in-state and hit Penn State or Pitt or something similar, I will be paying maybe 50% of her costs. If she goes pre-med or pre-law, she will be on her own after the first 4 years.

At a smaller, in-state school, I may be able to swing 75%.

If she decides to backpack across Europe for a few years, she is on her own!

My parents set up a mutual fund for my grandmother's estate to pay for school and then in HS I worked my ass off to get a good scholarship for full tuition despite all of that and working paid internships I still left college $7k in debt. I don't see how you can expect a kid to pay their own way thru college with the current cost of college. So I would say option 2 is probably the correct one provided they go to college for a degree that as potential to get a job when they get out and they are willing to try to find scholarships on their own. Also my parents told me what I had in the mutual fund so I knew what I would have to spend any past that was on my own. As far as grad school, if they aren't getting that paid for by someone else they are doing it wrong.

xflowgolf wrote: 1) I believe the parents should foot the bill for all college and college related expenses for their kids. 2) I think parents should help, but a full ride is a bit much. Maybe cover most of tuition (or community college), but they're on their own for room and board, but you can live in the basement for free. 3) Want to go to college? Do it yourself. When I was a kid we walked both ways up hill in the snow to work in a coal mine. Student loans exist for a reason. Get a job. ...or somewhere in between?

I am somewhere between #2 & #3.

I suppose if I was very wealthy and could just write a check, I would. But I'm not. So, I insist my kids have some skin in the game. I will assist them in their effort to succeed with enthusiasm commisurate with that effort. I don't believe anyone who isn't risking something is going to put in their best. Human nature... you don't appreciate the things you don't bleed for.

I just graduated in May. I probably paid about 65-75% of my way through working (Caddying in the summers, reffing hockey year round, shoveling snow, yard work, etc.), and scholarships--this accounted for maybe 10% of the total cost of college. My parents picked up the rest, no questions asked. As long as I was working myself, they'd have paid anything I couldn't. In reality, they paid for more than that 25-35% that I couldn't, as they also paid for my car and insurance.

For those of you who say "you want it, you can work for it... I did it!", how much did college cost for you? My parents both were able to go to a private school and pay for the entire cost working in the summer. That is realistically no longer possible.

If the parents CAN pay for their child to go to school, and the kid is a hard worker and working themselves, then the only reason not to pay for it is selfishness. It is 100% pure selfishness not to help out. I don't care if it is an interest free loan, a gift, whatever, help them out as much as is possible.

And before anyone says student loans, would you ever recommend that an 18 year old without an education and without a career take on a mortgage, or take out a loan for a new Lexus?

Oh yeah, grad school is on your own. I expect my dad will help me out though since there is still money leftover in the 529 plan.

Even if I was capable of paying 100%, I wouldn't. As GPS says, she needs to have some skin in the game. However, I want to encourage my kids to go to college, and I definitely don't think requiring them to pay for it themselves is a good way to do that.

Dear Daughter #1 is an excellent student. She opted to go to our local state university in their honors program, and she gets approximately half her tuition paid for via a merit scholarship. It was her second choice school, but her first choice would have cost more. I could afford to pay the rest, including room and board, at this school. However, with her buy-in, she is borrowing $2500 a year for undergraduate expenses, so that she has some ownership of her own education. She will get out with $10,000 in loans, which is enough to teach responsibility, but not enough to cripple her at the outset.

In her chosen fields, she will almost certainly need to go to graduate school. She's going to be much more on the hook for that, possibly even 100%. DD#2 will be entering college just as DD#1 gets out, so I don't know how much I will be able to help her with grad school. She also has a part time job, which right now funds gas money and other expenses. I imagine she will have to pursue TA and research assistant opportunities in grad school.

DD#2 is not as strong a student. College, and costs, are much more up in the air for that one.

Somewhere between 1 and 2 with a lot of "it depends". I've got four of the little beasts between the ages of 5 and 10. I could conceivably have all 4 in some form of higher education simultaneously. I think about it a lot.

We've been saving a couple grand a year for them since each was born. When it comes time for college they're going to have a pile of money and some choices. They'll probably be able to attend a local school and live at home and come away with money to spare. Or they could live away and go to a cheap school and eat ramen. Or they could apply to an ivy and start filling out a whole lot of loan/scholarship/grant applications. Along with all of that, we let them know that we will have discretion. You want to study theater abroad? Good luck. You want to study engineering at a good school and have the grades and work ethic to back it up? That is a cause we'll be willing to support.

All of my kids, even the five year old know they have college funds. It's going to be up to my kids to try and use them in a way that ends up in success. I'll let you know in 15 years how its working out.

Here in SC the lottery pays for in state tuition, so that will help a lot. There's some in a 529 and if all goes well I'll be able to put a bit more in it. She's going to have to bust her butt for scholarships and help pay her own living expenses unless she lives at home. So that puts me somewhere between 2 and 3.

It's no longer realistic for Mom and Dad to foot the entire bill unless they are wealthy.

I paid for my own. If I have children, I will definitely help with their expenses while in school.

Oh, here's the advice I got from professional counselors concerning 529 plans: unless you can put away almost everything you're going to need, don't bother. The first thing the financial aid office is going to look at is a 529 plan, and every dollar you have in one comes right off the top of anything they would have offered you.

We didn't have any specific plan for college saving other than to always put money away for savings at the rate of 15% of our income. As college loomed, we moved most of our liquid assets into annuities that tie the money up for 10 years, and make it invisible to the FAFSA.

Option 2 and 3 mixed. I did it, so can they.

My retirement comes first. If I can afford it then I will help pay for some school bills. I will not co-sign for student loans. I lived at home then got my own apartment, worked full time, and went to school at night. Yes it sucked and I didn't party all night and play XBOX all day with my frat. I busted butt, paid my own bills, and got a degree. There are tons of options out there to help pay for an education without going into stupid amounts of debt. I will gladly help my children apply for every scholarship in the books.

But no, I will not be blinding cutting checks to a college while hoping they get something useful out of the time spent there. Personally I think everyone should go to school for two years, then spend two years in their chosen major's profession, then finish up two more years at school. Learn something, apply it, then apply real world experience to learning.

mtn wrote: For those of you who say "you want it, you can work for it... I did it!", how much did college cost for you?

It's been a good while since I graduated college, but I think my loans were somewhere around $18-$20k when I was done. It'll obvious cost more when my kids go to college. However, at least so far, state schools and community colleges are still affordable. As I said, I definitely plan to help. But I firmly believe that having them work for much of it is as valuable a lesson, if not more so, than the actual education itself.

My wife went to Syracuse for grad school...all on loans. We were paying for that for years, it was a hefty chunk of change.

I plan to do something close to what my parents did, which was similar to option #2. My parents taught me to make my decision about college with finances in mind. Both of my parents worked while I was in high school (my mom stayed home when I was younger), so I wasn't going to get much need-based financial aid. I looked exclusively at colleges where I had a good chance of getting a merit-based scholarship. In the end, I went somewhere where I got a scholarship that covered tuition, my parents covered some of my room and board, and I had a very small loan when I graduated to cover the remainder of my room and board. I also worked while I was in college, roughly 15-40 hours a week while I was taking a full course load. All of my jobs were minimum wage, but it gave me some spending money so I wasn't dipping into my savings during the school year.

In the end, I got a great education for very little money, and learned some very important lessons about money. It was a good decision to pick a school that would allow me to graduate without owing a fortune, working through college instilled a good work ethic, and having a small loan when I got out prepared me for the reality of just starting out.

My brother went a similar route, he went to an inexpensive school and had some merit-based scholarships, my parents paid some, and he paid the rest with student loans.

When it comes to my children, I have a couple of key points that I'll use when they're ready:

I guess I pose this thread in part because I'm trying to figure this out for my own kids.

I'm still in the middle of my own pain... my wife is in school full time and is just finishing her Bachelors. We're racking up debt and paying a little as go on hers, but not much as she's otherwise been a stay at home mom while she has been in school.

My son just turned 4, and we have one more on the way. I disagree with my wife here, as she thinks she'd like to pay 100% everything, using logic around... happy thoughts, time to blossom, shouldn't be burdened, blah blah blah. It's also easy to think that while she effectively goes to school herself on loans and with me working and paying what we can from my single income.

I came from the opposite camp. I graduated from public university in '05. I did the community college thing then transfered to keep costs down. I worked a 2nd shift job all through the college (~30 hours a week driving a forklift) to pay my rent/cars/etc. Every summer I picked up an additional day job. I also shoveled with a plow crew at 3AM any night that it snowed. I paid for damn near all my own tuition/rent/etc. but I worked my ass off. I still managed to drink a few beers and have a good time. I finished with ~$5K in debt, which my parents paid off as a Job Well Done graduation present. They had the means to help me all along, but after I sluffed off and failed out my freshman year (wasn't ready to grow up), I chose to pick up the reigns and put my own skin in the game to make it work for me. I couldn't motivate myself on somebody else's dime.

I guess I believe in setting some set $$ assistance and being very clear about it. Basically saying I will pay for the equivalent of a community college the first 2 years and set them up with a car/computer,etc. Then 75% of state university upon transfer or something to that extent. The rest is up to you.. .and you can work while studying to emerge debt free, or you can finance that portion, depending how they decide to use their time. If you want to go to a private school, my assistance is a set $$ amount, the rest is on you. Begin the life lesson about debt, leverage, opportunity, etc. I also don't mind paying some assistance towards living expenses, again with some strings attached... defined amount, they budget additional, etc. I think if my kid earns scholarships or other earnings, I'll transition the $$ that was already set aside and still gift it as a first home assistance, or some other "investment" type gift that doesn't translate to an open spending account.

Now if my kid decides to go a trade school route and bypass college I'll fully support that path as well. Upon succesful completion, the same money and assistance is on the table along that path.

I'll check back in a decade... ![]()

93EXCivic wrote: I don't see how you can expect a kid to pay their own way thru college with the current cost of college.

I'm not so sure that the cost of college today is ALL that much more than when I was coming along ... sure in just the $$$ it is .. but then I was making $1.75/hr the summer between my senior yr in HS and my freshman yr in college ... pay after college was $2.50/hr ... income now is MUCH more ... and yeah I know I didn't have an apartment/townhouse, a car ( didn't get my first until I was in the Navy), a computer etc ... all those things that run up cost these days ... but I did work each summer from the 6th grade on, and saved most of it ( no cell phone bill, listened to AM radio, so their weren't any mp3/cd/pandora/whatever to pay for )

Parents AND kids seem to think these things are needs instead of realizing that most of them are wants

guess what it comes down to is how badly someone wants to go to college

wbjones wrote:93EXCivic wrote: I don't see how you can expect a kid to pay their own way thru college with the current cost of college.I'm not so sure that the cost of college today is ALL that much more than when I was coming along ... sure in just the $$$ it is .. but then I was making $1.75/hr the summer between my senior yr in HS and my freshman yr in college ... pay after college was $2.50/hr ... income now is MUCH more ...

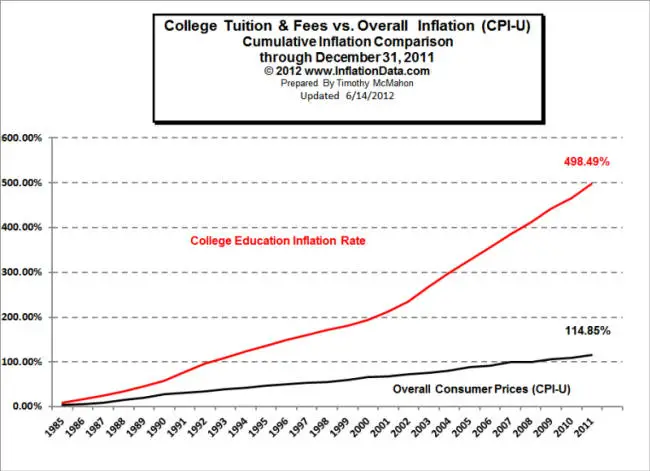

I'd have to disagree. Tuition cost inflation is absurd... compared to standard inflation (and therefore your earnings power).

I was able to pay my own way through college, but that was 35 years ago - as the chart above shows it's a different story for kids today.

wbjones wrote:93EXCivic wrote: I don't see how you can expect a kid to pay their own way thru college with the current cost of college.I'm not so sure that the cost of college today is ALL that much more than when I was coming along ... sure in just the $$$ it is .. but then I was making $1.75/hr the summer between my senior yr in HS and my freshman yr in college ... pay after college was $2.50/hr ... income now is MUCH more ... and yeah I know I didn't have an apartment/townhouse, a car ( didn't get my first until I was in the Navy), a computer etc ... all those things that run up cost these days ... but I did work each summer from the 6th grade on, and saved most of it ( no cell phone bill, listened to AM radio, so their weren't any mp3/cd/pandora/whatever to pay for ) Parents AND kids seem to think these things are needs instead of realizing that most of them are wants guess what it comes down to is how badly someone wants to go to college

Ok I went to a decently cheap school in a town with a huge focus on engineering because that would give me the best chance of having a career after college and I got a full tuition scholarship. It still cost over $55k to get thru college when you included a place to live (I split a three bedroom apartment cause that was about the best deal), the required meal plan (yes they required you to have a meal plan even if you didn't live on campus), full tuition only covered 15 hours a semester (and it was only good if you were full time and only lasted 4 years) and no summer courses, books and lab fees. $55k over four years isn't impossible to cover but that is providing you can get a full tuition scholarship.

A cell phone is required if you want any kind of social life whatsoever. That being said, a pay-as-you go is sufficient.

Meal plans are a complete ripoff. Wasteful and all of that whatnot. I always got the cheapest plan (I don't need unlimited meals). Eating in a normal fashion (2-3 meals a day, 1-3 meals out a month, and 1-3 meals a week of ramen/macaroni in my room) I was paying an average of $11 dollars a meal with the meal plan. For $11 a meal, I could have eaten out for every single meal. $22 a day for food is berkeleying ridiculous; heck, on my own I'd be surprised if I spend $30 a week in groceries. I'm probably at $50 a month including my beer.

mtn wrote: Meal plans are a complete ripoff. Wasteful and all of that whatnot. I always got the cheapest plan (I don't need unlimited meals). Eating in a normal fashion (2-3 meals a day, 1-3 meals out a month, and 1-3 meals a week of ramen/macaroni in my room) I was paying an average of $11 dollars a meal with the meal plan.

I agree. Unfortunately it seems that requiring them is becoming more and more common.

I went on the Wendy's Jr bacon meal plan lol.

93EXCivic wrote:mtn wrote: Meal plans are a complete ripoff. Wasteful and all of that whatnot. I always got the cheapest plan (I don't need unlimited meals). Eating in a normal fashion (2-3 meals a day, 1-3 meals out a month, and 1-3 meals a week of ramen/macaroni in my room) I was paying an average of $11 dollars a meal with the meal plan.I agree. Unfortunately it seems that requiring them is becoming more and more common.

That's happened to my stepbrother's daughter. She was required to join the meal plan. IIRC the whole deal was that since she lives in on campus housing the meal plan was included and could not be deleted. She told me a lot of the time she and her roomies eat stuff they buy at the grocery store.

dj06482 wrote: - Attending a community college for a few years isn't a bad way of figuring out what you want to do with your life, and then you're welcome to transfer where you want to go for the last two years. It's more important where you graduate from than where you started. This is especially important if you're not sure what you want to do with your life.

If my son didn't have clear goals - this is where he would be.

You'll need to log in to post.