I was debating starting this thread, but as it's technically a build thread and could contain useful information, I decided to go for it.

A little bit of background: When I was 18, I got my first credit card, and promptly maxed it out on stupid E36 M3. When I was 19, I managed to get a Best Buy credit card and do the same. Well, come age 20, I needed to come up with money to pay my car insurance, and really wasn't doing very well keeping up on bills already, so I took out an unsecured loan from citifinancial for way more than I should have, paid insurance and should have paid the credit cards off, then promptly lost my job and had to live off the loan money for a while. It got refininanced every couple of years as I'd not be able to make a payment. The credit cards went to collections, and started a fun game of harrassing phone calls, threatens of lawsuits, and my personal favorite, getting passed to different collections agencies and starting from the beginning again.

In 2011, I cashed in my UGMA college fund that I didn't use on college, and paid off my collections agencies, leaving me with only the loan payment. 250 a month, every month, that I'd been making regularly.

Finally, last year, my grandfather died, and left me a joke of a life insurance policy compared to what had been explained and promised, and that legal battle is still going on, but it let me finally pay off the citifinancial loan.

All told, 10 years, and almost 40 thousand dollars to pay off $3500 in credit card debt and ~$9k that the personal loan had grown to. I decided berkeley credit at that point, but reality doesn't always work the way we expect.

I've been keeping and eye on my credit karma though, and watching those two useless scores raise, level out, then begin to drop.

Earlier this week, I took a trip to my credit union and got started with a secured credit card. It has a $500 limit that I had to prepay, and only 12.99% interest rate that I find absolutely amazing compared to everything else I've been seeing or ever had that was in the 20%+ range.

The caveat of this card is that I HAVE to spend 150-300 per month on it(not gonna be hard with the work I have planned for the Miata), and wait to get the bill to pay it. Not a big deal waiting on the bill, 0% interest UNTIL a payment is late. This card also has the benefit of being reported to the credit bureaus EVERY month instead of just a few times a year.

I have not received the card in the mail yet, but logged into creditkarma just the same this morning, to see that my Best Buy card is officially off my Transunion report, and my score bumped up 60 points because of that. Leaving my Transunion at 637 and my Equifax a 639.

Most places that run your credit DON'T run those two specific agencies, but it gives me a good idea where I stand. Still technically "Poor" credit, but just barely below "Fair" which is 640.

I don't have crazy ideas about mortgages or car payments, at least not yet, but I want to get my credit somewhere respectable, so I can rent a car or get an Amazon or airline credit card and at least recover a little bit of what I spend.

I'm probably just going to post monthly updates to keep a record for myself, but I will happily answer any questions or hear about your experiences with this. This could also serve as a warning for those of you with kids entering the credit arena, although things aren't quite as screwy as they were back in 2005.

For a short term goal, I'm trying to get my credit rating high enough that I can take out a loan to EITHER buy a lift OR pour the concrete for my garage build. By spring, when I see that becoming a reality, I will already have plenty of cash saved up to pay for it, but in an effort to keep my credit building, I want a loan. Whether it's secured or unsecured shouldn't matter if I have the cash to back it up.

Welcoming all suggestions, questions, and complaints.

A quick way to build history is that for anything you are going to buy with cash, put it on the card and the next day you pay it off. It shows a history of using the credit responsibly. That can help build up the score.

In reply to Wxdude10:

That actually won't fly with this specific card, cause that was kinda my thought. When they send me a bill, they report it to the credit agencies, according to the loan officer at the CU. If I pay it off before I get a bill, it doesn't appear or won't help as much or something along those lines.

The blowoff job I picked up this week will pay me about what I need to be revolving every month, but I was told multiple times I NEED to wait till I get the bill to pay it. I have direct deposit setup for the job, and once the billing date is figured out, I'm going to setup autopay, pretty much just let it take care of itself. Not a big deal, 25 day grace period from the day the bill gets delivered, which means no interest. Just means once a month I order in some parts until I go in and increase my credit limit.

That is another benefit, to me, of the secured card is I control the credit limit. So if I decide one month I need to make a big purchase(like a bushing kit), I can go in and raise my limit up to cover it so that I'm staying around 50% utilization.

I prefer just doing everything with cash. Working for it, paying bills with it, etc. but that is kinda frowned upon in the world of today.

Very brave posting this. Good job on getting yourself straight.

Can you arange for the CU to do auto pay for the full amount on the due date?

Id stay with the CU for the slab/lift loan.

I 100% dont agree with the Dave Ramsey philosophy that your credit score doesnt matter if you don't use credit. One day you may want a mortgage and more importantly credit score can affect your ability to get a job, insurance rates etc.

Good luck

Good job. It's amazing how many people use credit without realizing the sorts or affects that is has on their financial life. My wife and I use credit that charges less than the rate of inflation. That's CC that are paid in full every month (0% plus 1% in Amazon points for us) and car loans below 2%. We're done with mortgages so this keeps our credit scores very high which helps with insurance rates and continuing to keep future credit cheap.

In reply to Adrian_Thompson:

I see Dave Ramsey as simplified answers to complex problems.

But, it can be a good plan when a plans is needed. From there, grow into a more complex plan.

To the OP, I came in to suggest picking up Dave Ramsey's book from the library (free).

My $0.02:

Get a good airlines reward card. Use it for absolutely everything you can and pay it in full each month. Make credit work for you. I pay 75 bucks for an annual fee for the card and take two international vacations a year with free airfare. Alaska Airlines (BOA manages it) pays ME to use their product and they make money of my interchange. It's a win win and I dont give one E36 M3 that the big bank makes a buck because I do too.

I work in risk management for a bank some Im not in that side anymore but I have my lending authority and used to do credit risk strategy. You have to use credit to show you have good credit. Its that simple. I used to lower credit lines before the big crash in 2008 (Much to the confusion of some coworkers and customers back then) because the guy who has a $50k credit line on a card but just uses $2k a month and pays it off....doesn't need $50k of OUR money sitting around. It's not because we didn't trust them, they obviously had great verified income and credit to qualify for $50k on a credit card anyway but it just didn't make sense.It didn't affect their credit when we adjusted the limits and that kind of customer didn't need debt to available credit ratios padded any further. It frees up more money on the books we can lend to other people. If that guy NEEDS $50k at anytime he could still get it. That's the kind of dude that wants a $50k credit line for their ego and it just doesn't happen as much as it used to.

I make sure that my bank doesnt give me automatic credit line increases either. We keep a $10k max limit on our cards and don't want it creeping up from there so I call and set it to stay there.

Use 1 card but have maybe 2-3 with no balance as a backup. When you just use 1, you are concentrating those points/rewards on 1 card instead of spreading them out.

Check your credit from the three bureaus and dispute any discrepancies. Get the free one from the government and don't bother paying for them so you don't get roped into monthly credit monitoring you dont need.

In reply to crankwalk:

I wasnt going to suggest that in this case but this is sort of what we do. Inst of a straight airline card though we use FlexPerks Visa through USBank. The advantage over an airline card is you can use it for any airline and its not X points = a certain type of flight (domestic or trans Atlantic etc.) Its X points = any ticket up to a certain face value. And if you dont quite have enough point you can pay the difference much more easily than airline cards where its expensive to buy more miles. Even though its a normal rate card weve never paid interest ever. With family in Europe its a flying spaghetti monster send.

RevRico wrote: That actually won't fly with this specific card, cause that was kinda my thought. When they send me a bill, they report it to the credit agencies, according to the loan officer at the CU. If I pay it off before I get a bill, it doesn't appear or won't help as much or something along those lines.

That doesn't sound right, but it kinda a sounds like the myth that's being peddled about carrying a small balance (ie, not paying the card off in full) improving your credit score. Which is actually not true.

FICO doesn't publish their exact scoring model, so what's known is by observation and experimentation, but that was good enough for a lot of people to figure out some strategies on boosting the credit score.

Basically, the important things are:

Does this card automatically "graduate" to a non-secured card after a specific time period? If not I'd keep an eye on the score (which it sounds like you're already doing using creditkarma) and once you get over 700-720 I'd apply for another, unsecured card.

Personally, I'm not a big fan of airline rewards cards unless you a) fly a lot (ideally with a specific airline) and b) get additional perks that you wouldn't get otherwise. Frequent flyer miles are getting harder and harder to redeem, so the miles one collects aren't necessarily worth the money you have to run through the card each and every month. Mind you, some of the non-affiliated travel cards might offer better deals. I prefer straight cashback cards, at least with those there isn't much of a redemption problem ![]() .

.

Regarding credit limit increases - I would suggest people take them when they are offered. A big part of the credit score is the amount of available credit and that's easier to keep low if you have more credit as long as you're confident you're not going nuts spending all the extra credit just because it's there. Doesn't strike me like that is going to happen, though.

To show how important available credit is - with the messed up switchover from Costco Amex to Costco Visa (Amex reported as closed and the Visa allegedly not starting to report until September) and my wife parking her tuition on one of the cards for a couple of months until the MR2 was sold, my scores dropped by about 60 points overnight. That was with total utilisation still being below 30%, BTW.

Edit to reply to Tim: after a year, I'll have the option of going to a regular non secured card. Unless I see a secured card hurting me,I might not upgrade,and just increase my limit myself. I'm not the most financially responsible person, obviously, so I'd rather have full control of my risk.

Those are some good tips, but way down the road for me, at least credit wise.

I don't fly as much as I used to, but was still planning on,and once my credit is good enough and I have enough income on the books, to get my preferred airlines(United) credit card. Even if it's not for vacations, it would sure be nice not to have to buy a ticket to fly and drive a car. Or get to the challenge cheap.

Right now is still the very early stages of the rebuild, and while I know most of what needs to be done, it's going to be sticking to it that's hardest for me. That's the part of all my plans and adventures I have issue with.

Along with this credit rebuild, I'm working with my accountant to turn my cash income into "working" income, meaning I have proof of income to show to credit companies and the like. It's a pain in the ass, but a good friend of mine grew up to be an accountant, so he handles most of it.

I mention that because proof of income has a lot to do with available credit as well, and my current blow off job only pays 100 a week. Not exactly enough to get anything useful credit wise, at least not now.

The IRS is happy with me, they get money from me every year one way or another, but that doesn't translate to the type of income requirements wanted by credit card companies and banks. Telling I don't know, visa, that I make 30k a year but only having pay stubs for 6 grand leaves them thinking I only make the 6 grand, despite paying the IRS for the 30 I do make. Means, to me, I need to push past my caps on the website, or work my cash income through the website and take on a self employment role.

I generate the majority of my income myself,and doing whatever comes along. This summer, for instance, I've been flipping riding mowers on craigslist and emptying out an estate on eBay/cl/depop/letgo. I've made a good bit of money, and the irs will get their cut come April, but that income isn't reflected anywhere credit sees it, which is a problem when you want credit.

RevRico wrote: Edit to reply to Tim: after a year, I'll have the option of going to a regular non secured card. Unless I see a secured card hurting me,I might not upgrade,and just increase my limit myself. I'm not the most financially responsible person, obviously, so I'd rather have full control of my risk.

I would check on Credit Karma or annualcreditreport.com if your secured card reports as a regular card or a secured card. Secured cards from banks usually report as secured cards (which isn't as beneficial for your credit as a "regular" card) whereas the ones from CUs can report either way. If it is reporting as a secured card it might be a good idea to switch to a regular card.

Well, the credit card came in the mail today. I'm not even tying it to any accounts until I get my cash reserves built back up some more.

Unfortunately, I think I've found it's first few months of purchases already. Wheels for 260, followed by tires for 320ish, to give me a full set of wheels and winter/offroad tires for under 600.

As much as I hate PepBoys, their Proline Wheels being buy 3 get one free is a godsend.

Woke up to an email from CreditKarma this morning, noting changes to my credit report.

My TransUnion score, useless as it may be, has bumped to a 689 JUST by adding the credit card. I wasn't expecting such immediate results, now if only places other than payday lenders actualy checked that score...

That's part of the whole sham of credit that I berking despise. There is somewhere in the neighborhood of 50 different reporting agencies. And they all have their own methods, algorithms and scores. There are the "big 4", Fico, Transunion, Experion, and Equifax. Each of those owned by a different credit agency, with no real regulation or rules regarding how things are measured. Meaning the numbers only mean what they say they mean. It's almost as frustrating as fractional reserve banking when you're trying to use logic and common sense to figure it out.

That said, I purchased wheels yesterday on the card, and will be depositing the payment in my bank today on my way to work. I won't be paying the balance until I get the bill on the 15th just to play nice with what the CU says I should do, but the money is already there so I don't need to worry about it. Unless I get really antsy for tires, in which case, I'll carry that balance to the end of the month and pay off the wheels now.

I can appreciate shills with methods and books about it, because hey, everybody has to make a buck, but this is one industry where you HAVE to take EVERYTHING with a grain of salt. Much like banks, credit companies are labrynths of paperwork and special definitions, and NEVER have your best interest in mind. What may work with a few agencies can screw you with others, so a new part of my homework is researching what banks/agencies use which reporting company, to then decide the best way to go about this.

I'll be curious to see come September when I pay the bill what changes have been made across the boards.

Edit: Discover cards "Free Fico Credit Report Card" is useless. Refused to let me sign up a month ago, and now says my email is already registered until I hit lost password when it tells me I don't exist. With no contact or support help. Typical.

FICO is a software company that just cumulates credit scores from the 3 major bureaus. It's not a credit bureau itself.

In reply to Adrian_Thompson:

Manual underwriting is the method for securing a mortgage without a credit history. The loan officer has to "manually" review the borrower's financial history (employment records, bank statements, income tax returns, etc...). In other words, they verify that the person borrowing the money has the ability to pay it back. Done correctly, this protects both the lender and the borrower from making mistakes. ![]()

A zero credit score is OK. A low credit score is not. The insurance companies do tend penalize folks with no FICO score, but that is a minor issue compared to being in debt.

Full disclosure, I personally do have a credit score because I have a mortgage and a card issued by work. If not for those, I would not have one. I drank the Dave Ramsey "coolaid". I had the typical "good debt", car loans, student loans, etc. It took a while to dig out and get debt free, but it is absolutely worth it. It gives you options.

A funny aside, the autocorrect makes "coolaid" into coolant if you don't force it with " ". ![]()

Wow, guys, very informative thread. Thank You.

Observation:I am financially very conservative. Not Dave Ramsey crap, but pay on time, zero c.c. balance on a card that is my primary spending device, financed a motorcycle, paid it off early, home loan, on time. In short, I am responsible.

I have a friend who is not. He transferred funds from card to card, lives on the edge, works little, spends much, and is often in arrears. He does come from wealth, but let's leave that aside. He recently sold a house well, and was able to pay all c.c. debt off, and his credit score instantly jumped from half of mine to equal (very strong). So, history has little to do with it. This is very good for people who slip, and not really bad for me.

This leads me to a question. Because I'm tired of being a chump, can someone explain the whole cash back thing to me (a layman)? I don't fly enough to need miles, but I see other people working the system to their advantage, and sometimes wonder why not me.

Not to go off on a tangent, but I'm not finding where dave Ramsey talks about "good debt."

In fact, I found him saying there is no such thing.

I agree that debt is never a good idea and really hand it to the op for stepping away from it and working hard to pay with cash.

Awesome thread OP. I second the airline card and recommend SouthWest's option. They have a hub in Atlanta which is great for fly and drives.

crankwalk wrote: FICO is a software company that just cumulates credit scores from the 3 major bureaus. It's not a credit bureau itself.

This is from Discovers website advertising their free FICO score

"It's a three-digit number that summarizes the positive and negative information on your TransUnion credit report. FICO ® Scores are the most common credit scores used by lenders to quickly assess your credit risk, and it can influence everything from car loans to mortgages to credit cards."

So how the hell is it different than just a Transunion score? Stupid credit agencies. TransUnion is now a 690, high side of "Fair", so I'm assuming FICO is close to it.

Only a small update, but an update none the less. My CreditKarma reports just updated, and both Trans and Experion are showing the new credit card. No balance reports, but holy points jacking. Experion went up 73! points just for opening the account, putting it into "good" territory at a 712.

I can't believe JUST opening an account can have such a major impact. I still haven't gotten a bill yet, so no usage has been reported to the agencies I guess, but it will be interesting to see how it changes over the next year with usage and proper repayment.

So I've not updated this in a while, and with a new month and new scores, I thought it was time.

My score took an immediate nosedive the first month of using the card because my balance was on the high side when it got reported. I guess that's the only time they care, because I've spent almost 2 grand through this thing in 3 months with my $500 limit. Buy stuff, pay it off, repeat.

That said, transunion has gone back up to 680 with the most recent report to them. Amazing what going from a 75% credit usage to a 12% credit usage can do.

I think a big key to this that I haven't found yet is what day of the month the data gets reported. I'm doing what I can to keep active balance under $100(20% usage), but it's tricky when it takes 3 days for a payment to clear, and 5 days for that balance difference to appear in my savings account.I should keep a ledger, apparently.

This adulting crap sucks, but it is showing promise. In addition to credit card offers appearing in the mail, I'm now getting them for cars(at ridiculous rates). Hopefully, this will be able to translate to decent loans for repairing the house or buying cars I the nearish future.

Congratulations on your success. Maybe I can help inspire you.

9 years ago I was going through a divorce and living off credit cards because she emptied all the accounts. Missed a lot of payments, paid a lot of ridiculous interest, etc. My credit was under 500.

Fortunately, Discover never cut me off, and I used it to rebuild. It's tough to learn to game the system, and each website has different and conflicting advice.

But I'm not here to offer advice, just inspiration.

Nine years later, after some stumbling and learning how to play by their systems, I've pulled 3 scores: Discover/Fico, Quizzle.com, and my CU also gives me a score every 3 months. right now, those numbers are 829, 815, and 845.

So it takes time, don't rush it, but it is very achievable!

I used this forum about 6 years ago to help me get some young mistakes off my credit from when I was 18 (27 now). Very imformative. I know those FICO scores tend to be 30-50 points below what the "free credit report" companies. My take on credit is, it makes no damn sense but you shouldnt try to make sense of it. Just play the game and use it to your advantage WHEN/IF you can.

Best thread I've read in a long time. Learned a Lot.

RevRico wrote: So I've not updated this in a while, and with a new month and new scores, I thought it was time. My score took an immediate nosedive the first month of using the card because my balance was on the high side when it got reported. I guess that's the only time they care, because I've spent almost 2 grand through this thing in 3 months with my $500 limit. Buy stuff, pay it off, repeat. That said, transunion has gone back up to 680 with the most recent report to them. Amazing what going from a 75% credit usage to a 12% credit usage can do. I think a big key to this that I haven't found yet is what day of the month the data gets reported. I'm doing what I can to keep active balance under $100(20% usage), but it's tricky when it takes 3 days for a payment to clear, and 5 days for that balance difference to appear in my savings account.I should keep a ledger, apparently. This adulting crap sucks, but it is showing promise. In addition to credit card offers appearing in the mail, I'm now getting them for cars(at ridiculous rates). Hopefully, this will be able to translate to decent loans for repairing the house or buying cars I the nearish future.

You should never ever need to take a loan out to repair your house... (unsecured debt is ~9% plus for me with 840 score...)

Also you will not see those ridiculous rates come down until you are in the 750 rate range... Watch your score in January, it should get a small bump due to it now being a fiscal new year. (I think).

You need time, like another full year to really see the benefits. It's slow going and annoying but totally worth it.

Your score dived because you had horrible credit and now showed a balance. As your credit history gets longer w/o issues the less likely it will "dive" due to a balance being there. I'd ponder a new card when you hit 700+ rating. Something with a higher limit. Spend as you do now, but it'll show better restraint than one with 500 bucks as the limit. (Though That's my gut feeling there.) Keep the first card open and only use sparingly so that you have an older account in the history.

If I am reading correctly, you are doing some wise spending on your only credit card and then paying it off before the interest hits. This "activity" earns you a good score showing that you can use credit responsibly. The risk being that you are gambling that you will remembering to pay and they are wagering 20% that you will not remember.

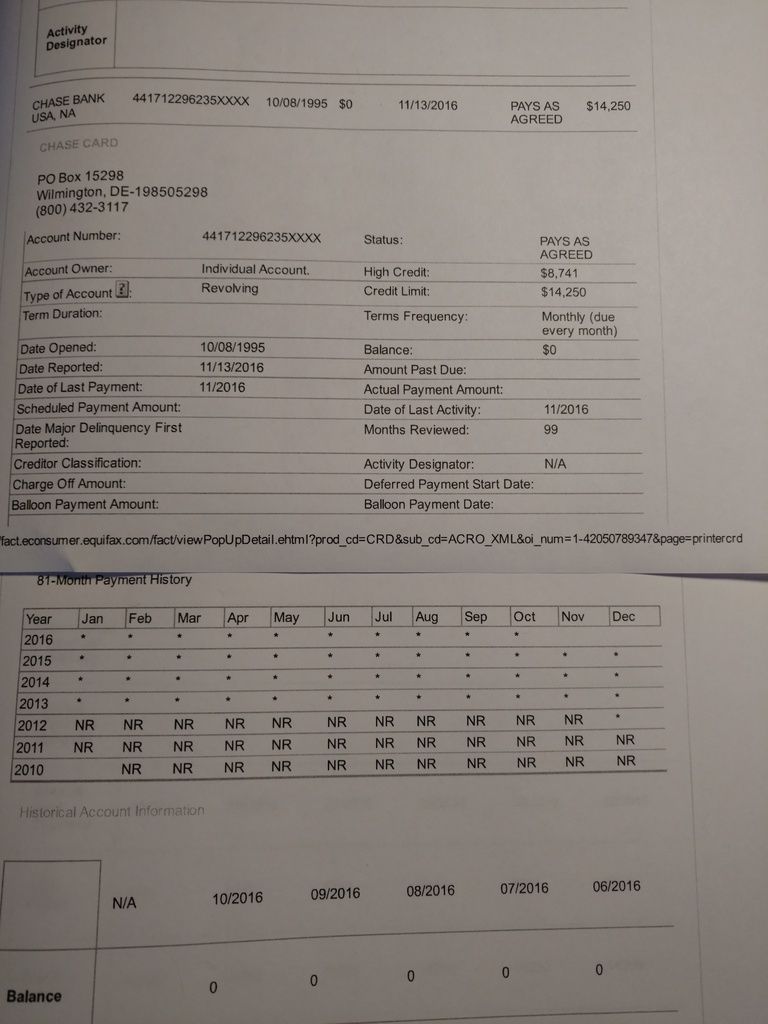

Here is a trick that I do and I swear it works. It also eliminates the risk. I have a Chase Account that I never use. I mean never, like I don't even keep the plastic card on me. But, every month, I send Chase a $5 payment for that account. This then builds me up a positive balance. The banks don't like you to have a positive balance so when it hits about $50, a letter arrives from Chase and in it is a check for my $50. This eliminates the positive balance and I have all my money back.

The win here though is that every month Chase sees that I have "Payment Activity" and every month they report on me favorably. I just went to the free annual report and pulled a report. I took a picture on this specific Chase account.

NR= Not Reported (which is the same as no activity) Since Dec 2012 Chase has reported on me every month and I have bought nothing. Date of last payment was 11/2016 (last month) I have not bought anything with this card in i'll bet 5 years but I have been sending them $5 since Dec 2012

2012.

So, my advice is give it a try. Get to a zero balance and then keep sending them $5 every month. Eventually, they will send all the money back to you. All the while, you will look like a stellar customer. In addition, you will have zero risk that they will hit you with 20%. I did not get a FICO score when I pulled this recent credit report but just so you know, last month I secured a used car 1.99% loan with just a phone call. I know I am good.

Another benefit of these small payments is that the banks tend to lower available credit or close accounts on accounts that have no activity. These $5 payments keep these lines of credit open for me and show that more creditors think I am worthy. I send the payments electronically through my scheduled online banking and I never even notice they are sent. If $5 is too much, send $2.

Edit: I'm adding in an update here for Sept 2019.

I still send these small payment to my Chase Card (officially J.P.Morgan Chase Bank.) Still, to date, I have bought nothing with this card and I do not keep the plastic with me. Here are some screen shots of a current credit report .

I wrote above that I have been sending them $5 payments. Looks like the reality is that I send them $10 payments. Either way, the story is the same, every couple of months I get a check back from Chase which is returned payment for positive ballance with them. I get every dollar back.

Chase thinks (and reports every month) that I am a wonderful customer. This keeps $14k worth of credit open to me that would otherwise be shut for non-use. I also think it makes my percentage of debt vs available credit used look very favorable.

You'll need to log in to post.