In reply to ProDarwin :

The implication is that you don't HAVE the cash.

If you did have the cash, even if you got a loan at 5%, there are few investments you could do with the cash that could beat that guaranteed. If there were, take out the loan, make the investment with THAT, and buy the toy in five years.

Given a low enough rate, I prefer to play with the bank's money than my own.

I have in the past, but that ws a long time ago. These days I'm in the debt-averse group. For just about any purchase.

Pete. (l33t FS) said:In reply to ProDarwin :

The implication is that you don't HAVE the cash.

I disagree. It is unclear, hence the wide range of answers.

Pete. (l33t FS) said:In reply to ProDarwin :

The implication is that you don't HAVE the cash.

If you did have the cash, even if you got a loan at 5%, there are few investments you could do with the cash that could beat that guaranteed. If there were, take out the loan, make the investment with THAT, and buy the toy in five years.

With todays rates, if your credit is so poor you're getting 5% on a vehicle loan, no, you shouldn't be financing it.

Anything under 84 months is sub 3% at PenFed.

ProDarwin said:OP question: Would you finance a fun car purchase?

It seems what most people are answering is: Would you purchase a car you couldn't afford to pay cash for?

My answer to both is more or less the same, but the second one is much more reasonable to say "no" to. Also not the question being asked, as you pointed out.

Pete. (l33t FS) said:

If you did have the cash, even if you got a loan at 5%, there are few investments you could do with the cash that could beat that guaranteed.

Disagree. For one thing 5% is high these days, 4% or lower isn't hard to do even on a private party purchase. My moderately conservative investment account has been making 8-10% even considering.....whatever it is the economy has been doing the last 6 months. It's not quite guaranteed, but any half decent investment will pretty easily clear 5% returns over the course of a typical auto loan, barring pretty much anything but a complete economic collapse.

The invest with the banks money makes mathematical sense at a low rate if indeed we are wisely investing the other money. Usually this theory just leads to spending more money on other junk we don't need instead of continuing to save and invest.

I'll always be on the pay cash side for toys and pay off your house early side of the equation.

ShawnG said:Never take out a loan on a depreciating asset.

Full stop.

I've absolutely never understood that mentality. By extension of that logic you should never buy a depreciating asset at all.

You just need to consider the interest paid as part of the bottom line total price you decide to pay.

Duke said:ShawnG said:Never take out a loan on a depreciating asset.

Full stop.

I've absolutely never understood that mentality. By extension of that logic you should never buy a depreciating asset at all.

I understand this mentality, assuming you don't have the cash to payoff. A car can depreciate faster than you pay it off, leaving you stuck with it. I've seen this happen to people before. They have their finances stretched and selling the car would be ideal, yet they can't because they are $2k upside down on the loan.

I cant finance a car for myself. I tried it and it absolutely crushed any enjoyment I had since it didnt get driven much but every month I had to make a payment regardless. Sold it within a few months. If you want it bad enough to drop a large amount of cash on it, it's more likely you will enjoy the ownership experience and not worry about the financial aspects.

Fun car that car that is going to be my daily driver? - I'd consider it. I've done it before, but it was in my early-mid 20's when it was more difficult logistically and financially to have a dedicated fun car separate from a DD.

Fun car that isn't a DD and/or gets seasonally stored? - No. My reasoning here has more to do with insurance. Every bank/CU I've had a car loan with required that I have full coverage insurance on that car for the duration of the loan. While I don't have a problem with this, I'd rather not spend the $100+/month for insurance (plus the car payment) for something that would be sitting in my garage for Michigan winters that last anywhere from October to May.

There are a lot of interesting points here!

To be clear, yes I was asking "would you rather finance than pay cash, assuming you had the option of either". But there are many people who have no issue financing a fun car with money they don't have yet as well, and while we seem to have less of them on this board, I'd be interested to hear that perspective too.

I was talking about this recently with my dad, but in terms of houses. His argument was that most houses will at least keep up with inflation, and many will outpace it by some. So therefore, if you have a 3% loan and the house is gaining value at around 3% or better each year, you are effectively living there for free (assuming you can keep up with the cash flow needs to service the loan).

Assuming that they can afford both, many people choose to live in a 250k house over a 150k house, meaning the 100k difference is 'fun house' money. In the end, when they leave and sell, both houses have left the owner 'even' (minus any expenses for running the house like utilities and upgrades/repairs), but one got to enjoy a nicer house for the entire period.

The crux, of course, is that the higher monthly cash flow needs of the 250k house have opportunity cost during the time of ownership. But that is simply choosing to live in a nicer house over choosing other possible luxuries to purchase.

Since financing a big portion of 'fun house' is common, I was wondering if people feel largely similar about financing a big portion of 'fun cars'.

Here's another analogy. Say you want to buy x car for $10k. Let's say this car is unlikely to depreciate or appreciate much going forward, but will keep up with inflation. Let's also say that you will keep this car a long time.

Option A: buy car now with financing - Option B: buy car now with cash - Option C: take time to save up cash and buy later with cash, assume this would take 3 years. All three mean that you will end up paying a very similar amount of money for the car in the end. A = 10k +interest rate%, B = 10k +opportunity cost of x%, C = 10k + ~3% inflation over 3 years.

Whether Option A or B is 'better' really comes down to interest rates and investment returns - which is very much a personal belief/situation as to which is more beneficial.

But the big bummer is that Option C means you will own and enjoy the car for 3 years less in your life.

I think 3% increase per year on the value of a house is on the optimistic side, but there are so many variables in play that in some locations that could be high or low. For my personal projections I usually assume 1% and allow myself to be surprised if I have to sell a house and I walk away with more than I expected.

If we apply the same "need" requirement to the fun car as we would a house, because housing is a "need" to be fulfilled... depending on the situation a fun car can very much fill the need for transportation. If I'm single it's easy to justify financing a Miata, because it's a fun car that can also serve my need for basic transportation. I might also be in a position that a newer, financed Miata with a warranty might be a better choice than a used one I can pay cash for, as I've had jobs that were so demanding that I didn't have any extra energy left to tend to the needs of an older car.

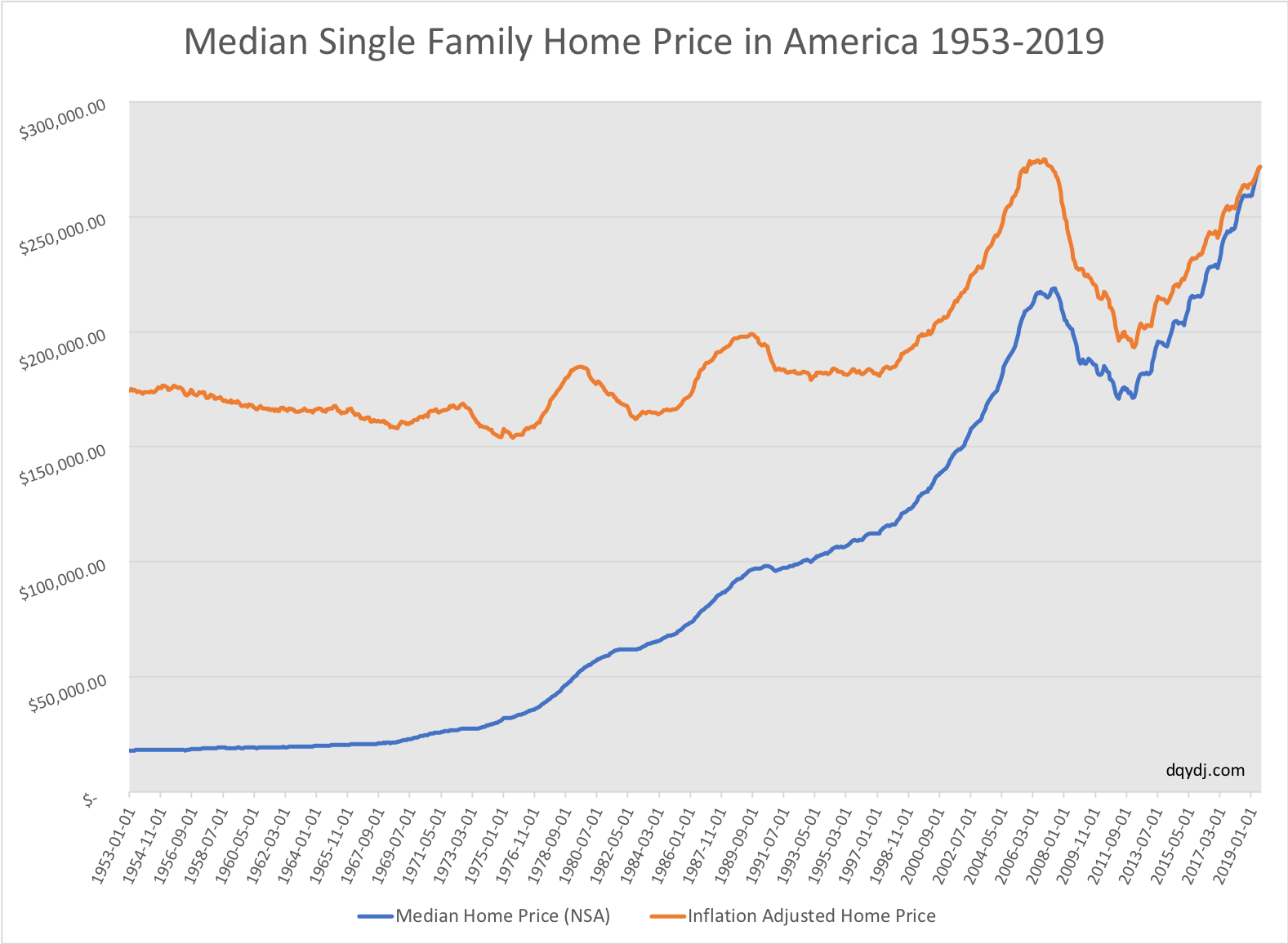

https://dqydj.com/historical-home-prices/

Check out the inflation adjusted home prices (orange line). You can see that homes basically match inflation or do slightly better, on the mass average. They seem to be high right now.

z31maniac said:Pete. (l33t FS) said:In reply to ProDarwin :

The implication is that you don't HAVE the cash.

If you did have the cash, even if you got a loan at 5%, there are few investments you could do with the cash that could beat that guaranteed. If there were, take out the loan, make the investment with THAT, and buy the toy in five years.

With todays rates, if your credit is so poor you're getting 5% on a vehicle loan, no, you shouldn't be financing it.

Anything under 84 months is sub 3% at PenFed.

This. I JUST financed the FoRS at 3.9 through my local bank. Penfed was lower but I'm happy to pay the additional pennies to talk to someone who speaks English as a first languange and be able to have face-time with someone 5 minutes from my house.

Very few people look at the total cost of ownership on anything and car nuts are some of the worst. Of all my racer friends I think I'm the only one who tracks every penny (perils of being a Purchasing Analyst).

So with that said if you are tracking everything (as pointed out, the full coverage insurance etc.) and your cash can earn more, then it's not bad idea.

While I did finance a fun/toy car 25 years ago, I've bought most of them cash.

Not financing keeps the price down, very easy to spend 4-5K more then you would have if you were paying with hard earned cash.

Tom1200 said:Very few people look at the total cost of ownership on anything and car nuts are some of the worst.

House people are absolutely the worst at this.

When I was younger, I took my leased DD to the track and borrowed a couple cars. I was lucky nothing ever happened, but if any damaged occurred, I would have been on the hook for it. I would never finance a fun car unless I could get some extra rare car Ford Gt and be able to resell it for more. Otherwise fun cars are a dime a dozen under the mark of financing and since manual transmissions are easier to find on used cars, I don't see the point.

When I was younger and was building my credit history, yes I did. I was working with my credit union and it started with my first car. I had six months of steady work history and a deposit record of my pay checks. The key was starting very humble and working with the same institution.

I worked with them for a number of years and ultimately worked up to a series one Lotus Elan and the Sunbeam Tiger. The loan committee approved of my choices. They even went for the '73 Jag XJ-12. They liked my payment history.

Now I buy old cars, avoid the deprecation and have them as advertising my services. My accountant keeps it all legitimate.

If you are stressing about basses points in todays credit world you might never actually drive and enjoy your "fun car".

Robbie (Forum Supporter) said:I was talking about this recently with my dad, but in terms of houses. His argument was that most houses will at least keep up with inflation, and many will outpace it by some. So therefore, if you have a 3% loan and the house is gaining value at around 3% or better each year, you are effectively living there for free (assuming you can keep up with the cash flow needs to service the loan).

Assuming that they can afford both, many people choose to live in a 250k house over a 150k house, meaning the 100k difference is 'fun house' money. In the end, when they leave and sell, both houses have left the owner 'even' (minus any expenses for running the house like utilities and upgrades/repairs), but one got to enjoy a nicer house for the entire period.

The crux, of course, is that the higher monthly cash flow needs of the 250k house have opportunity cost during the time of ownership. But that is simply choosing to live in a nicer house over choosing other possible luxuries to purchase.

Since financing a big portion of 'fun house' is common, I was wondering if people feel largely similar about financing a big portion of 'fun cars'.

The house itself may keep up with inflation but there is also:

Insurance, property taxes, maintenance and repair, etc. Unless you're in a super hot market, it's unlikely you're actually making money on a house when you factor what it costs to actually keep it going.

But there are other benefits to owning vs renting that aren't strictly monetary. But something that costs you money should never be looked at as an investment.

ProDarwin said:Tom1200 said:Very few people look at the total cost of ownership on anything and car nuts are some of the worst.

House people are absolutely the worst at this.

I'd still rather own than rent, but the first time you're hit with a bill for a full HVAC replacement you start to question your priorities. This is why I'm fine with low interest loans on cars, because taking a hit like that is easier with a car sized cash reserve.

Robbie (Forum Supporter) said:This is sort of a poll thread, but also looking for the reasoning behind your answers. The simple question is, would you finance a 'fun' car purchase? Fun can mean just about anything, if you consider your daily driver to be your fun car and lease it for example, or if you want to buy a 1969 superbird with a specialty loan, etc.

So far, I have only financed one car in my life (and I've bought a lot of cars...). That one I bought for the purposes of business use, so really I've never financed a car except for maybe taking short term cash out of a heloc and paying it back in a few paychecks.

What do you do and why?

Yes I would and yes I have. Two reasons behind my past decisions.

1) The kids mom had little to no credit history and I wanted a fun car. Financed it her name, paid it off over a couple of years. It got her off on the right foot credit wise and I got a car I wanted.

2) Life is too short sometimes to sit around waiting. There are arguments of "if you dont have the cash don't buy it" and "you should play it safe and plan for a rainy day and retirement."

- 2a) I almost lost my life in a bad car accident at a young age. berkeley saving for retirement, you never know when your time is going to come. Life each day as if it's your last and have fun. If you have kids or a significant other be smart about it and make sure you have contingency plans for them in life but I'm not waiting until I'm 60 to have fun.

- 2b) I've lost too many friends at a young age to cancer, accidents, natural causes, etc. It's put life into even more perspective that waiting around to accomplish goals isn't always a great plan. I don't want to be on my deathbed saying "I wish I would have done x, y, z" I wanna say "I'm glad I did x, y, and z"

Moral of the story - there's no shame in financing something fun if that's what your heart desires. Just make sure it's still within your means.

...- 2b) I've lost too many friends at a young age to cancer, accidents, natural causes, etc. It's put life into even more perspective that waiting around to accomplish goals isn't always a great plan. I don't want to be on my deathbed saying "I wish I would have done x, y, z" I wanna say "I'm glad I did x, y, and z"

Nearing 60 years I've seen a lot of death and felt a lot of pain. Still, I don't regret anything I've done. Regret is for the things left undone and words not said.

You'll need to log in to post.