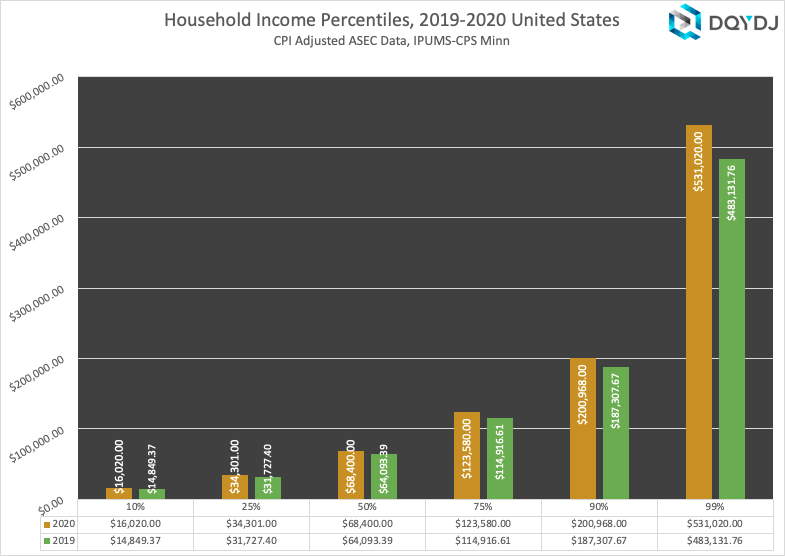

Median household income (50th percentile) was $68k for 2020. Since the "class" discussion is typically broken into thirds, with upper, middle, and lower I'd use the middle 33% to define "middle class". So 34th percentile starts around $44k and goes up to 66th percentile at $100k. This is household income, which may or may not include more than one earner.

Of course income is only a part of the puzzle, and how that translates to security, liquidity and net worth all matter too. I don't know that I could call someone that spends everything they make "upper class" regardless of what that income level actually was. And I don't know that I'd call a low wage earner "lower class" if they could comfortably support themselves and might one day be able to retire. So spending/saving habits seem like the second (and more critical) piece of the puzzle to me.

wae said:I remember there was an episode of the Cosby Show where Dr. Huxtable told his kid that the definition of "rich" was when your money worked for you versus you working for your money.

I agree with that 100%. When people ask me "why do you think we need to tax the rich" I make the distinction between working rich and non-working rich. Yes, I do think non-working rich should bare the largest burden of our taxes.

Having some intimate knowledge of how the later considers their finances, they give a tremendous amount of money to charity to avoid additional taxation, but as a whole, a few percentage points of taxation doesn't threaten them. They have such tremendous wealth that even at absurd levels of taxation they'll still make money doing virtually nothing. At those levels the theme of "money is no object" really rings true, especially when they themselves didn't necessarily make that wealth (generational/old money).

For the rest of us mere mortals, I know some folks who make above $200k/year but they work damn hard for it. Granted, it's not physical labor, but its a lot of time in airplanes, flying around the world, doing highly technical or tedious work when they are in the office, and sitting in meetings all day everyday. I give a lot of credit to someone who despite making more in a single year than I'll make in five, still goes to the office everyday at 8AM. Should that person still pay taxes? Yes.

I also know some business owners. This is where my views on taxation get a little bit hard to quantify. I give lots of credit to job creators, but I don't think every person who invests in a company is a job creator, and therefore, I have some concerns about saying that because someone is rich and doesn't do work, that they should get a tax break because their investments create jobs. Not necessarily. Real estate is a great place to make money out of proverbial thin air. There are plenty of other examples. Where I want incentives is for businesses and business owners to create good paying sustainable jobs. No, not just $15/hr minimum wage, but the local AMI rate. And it'd be rad if somehow we could tie the taxes of the ownership to the difference in incomes across the company and investors. If a business owners makes $100k but his employees make $80k, then I'd be inclined to give that business owner some serious tax breaks.

The thing that worries me the most is how the lower and middle classes just haven't seen big changes in their lifestyles in the last 30 years. Granted we all carry around mini-super computers that can get the world's information nearly anywhere, and we drive far nicer vehicles that 30 years ago, but our lifestyle hasn't change - ie, we still work 8AM-5PM, M-F, because we desperately need to maintain healthcare coverage, and we get roughly the same amount of vacation time we did 30 years ago, same amount of Holidays, and now, we pay significantly more of our household income towards housing.

And we're all mostly locked into that. Sure, some people could live off grid and only "work" a few hours a week to pay their bills, but for most people, even in places with very low cost of living, you still need some sort of steady income and more importantly, still need healthcare.

The "Middle Class" shouldn't just be about "stuff" it should be about lifestyle. If our lifestyles have drastically changed in 50 years since the middle class was coined, we need to revaluate that definition. If now it require two incomes to afford a house, and then we pay for childcare, and we pay higher amount for healthcare, then its hard to say that lifestyle matches that of the 1960s.

I'd like to see changes in country that allowed the middle class to live easier lives, with less stuff, and more time.

In reply to pheller :

I recall in high school we had an assembly where a 'futurist' came in to talk about the world we would be living in over the coming decades. This was the early /mid 80's. The thing that stands out most in my mind was how he kept referring to the coming productivity revolution, driven by robots and computers, meaning one of the biggest challenges my generation would face was how to spend our free time as technology reduced our workload leading to shorter working hours and longer vacations. Yeah, not quite!

In reply to Adrian_Thompson (Forum Supporter) :

We had exactly the same thing in the 70's.

I took an easy credit course called Futures where they talked about four day work weeks and a leisure society filled with spare time and polyester.

I actually enjoyed that course, though it was mostly fluff and nonsense

Adrian_Thompson (Forum Supporter) said:In reply to mtn :

We've had similar discussion to this on here before. I think it was something like 'what's you eff it I'm done' figure to retire and walk away. I've always believed it's around 20 times what you are happy to live on annual. That much should allow you live off the interest (including annual COL increases) without ever touching the principle. For some people that may be $500k, for others it may be $5m.

You'd be surprised at how many people say "just one more year" when they get to that point. In my experience, the type of people that accumulate above 25x their spending in invested assets (not net worth) are conservative enough with money that they still have a hard time walking away until a life event shocks them into it or forces it.

Adrian_Thompson (Forum Supporter) said:Here's another thought I've had I'd like people opinion on. I think one of the reasons that the vast majority of Americans say they are middle class may be that they judge themselves, in general, in reference to those they see around them and interact with. On the whole peoples friends, neighbors, colleagues etc. tend to be in similar socioeconomic groups. So if someone lives in an area where $100k buys a median house, and they and they're neighbors all drive on average a 10 year old pick up truck they will look around and say 'I'm broadly the same off as everyone around me, therefore I'm not an outlier so I must be middle class'. Someone who lives in a $500k median house area and everyone in their community leases a new Merc/BMW/Tesla/Caddy every three years will probably look around and say something similar and come to the same conclusion.

This is very true. I think it might also be that most people have a tendency to fully leverage themselves for the sake of lifestyle/status. The guy in the $500k house with a leased Merc and a country club membership is basically struggling the same amount to balance income and expenses as the guy in the $200k house with a Camry. They both struggle the same way. Now, the $500k house guy could live in a $200k house with a Camry and not worry, but then he'd be comfortably living a middle class lifestyle.

A bigger question is why the people living below middle class think of themselves as middle class. Perhaps it's a pride thing - at least in the US.

I know we're biased about cars here, but I think car buying ability is a decent measure. It's sort of a luxury/status thing, but it's also very practical on the verge of necessity. What would you be able to do if you needed a new car? Could you even afford a car outside a predatory buy-here-pay-here lot? Would you need to get a loan for a modest used car that would be a significant drain on your finances? (Lower-middle) Do you have options up to buying a new Camry/Accord level car with a loan that takes a bit of work to budget for? (Middle class.) Would buying an "average" new car be a pretty negligible expense?

mtn said:In reality, it looks like a very, very steep quarter-pipe.

FYI, the proper statistical term for that type of distribution is "skewed to the right".

Wearymicrobe shared that he's worth a little over 10 million...last time I checked, the top 1% had a net worth of 11.3 million so he's right on the number despite being worth many, many, many times more than the average person.

Call me obsessed but I calculate my net worth, to the penny, at the close of nearly every trading day....literally, if I buy a soda or whatever, I pull a buck fifty out of my net worth. At the end of each year I perform a calculation that I've never seen financial advisors do...I work out the ratio of organic vs inorganic growth to my portfolio. Organic = appreciation of my existing investments and inorganic = sweat effort coming from contributing to my 401K, paying down my mortgage, etc.

Over time, organic makes a greater and greater percent contribution relative to inorganic which I think is an elegant way of tracking progress towards becoming irrelevant...think about it, the goal is to make yourself irrelevant (i.e. current efforts are trivial relative to the gains you're getting from previous efforts).

Simply stated "time to retire" can be defined as the point in time where your efforts don't matter very much anymore.

I'm maxed out on my 401K contributions (including catch up) pay down my mortgage 24K per year (I currently owe 50K to the penny as I calculate carried interest each month to hit an exact number) and buy a little stock here and there. Still, my organic to inorganic ratio averages about 5.8 to 1.

I'll be 57 at the end of June and I think I'm on track to making myself irrelevant.

Beer Baron said:A bigger question is why the people living below middle class think of themselves as middle class. Perhaps it's a pride thing - at least in the US.

I remember a quote, someone once said: "The United States is a country full of temporarily embarrassed millionaires."

Everyone in my neighbourhood in B.C. Canada has a new truck or two in the driveway, new RV, new boat or motorcycle and a mountain of debt.

The only debt payment I have is my mortgage and my monthly credit card bill because I use it for everything. I didn't start out this way. I wasted WAY too much money in my 20s and spent all of it in debt to somebody because I was stupid with money.

My house insurance company was surprised when they asked me for a void cheque and I asked "what for?". It was for the monthly payments. I wanted to pay in full and they were very surprised.

I'd rather pay everything I can as soon as I can and deal with a month or two of suck than 12 months of suck plus interest.

barefootskater (Shaun) said:In reply to mtn :

Man I wish I'd have had someone like you in my friend circle when I was younger. I wasn't interested in the advice of boring old people, but I might have listened to someone in my own age group.

If you want, I can send you a document I've written up on this.

One other thing: If you value financial security for your kids and want them to build wealth, be prepared to help your kids when they're adults. That does not mean to let them be freeloading leeches and living off of your accomplishments, but there is a difference in a freeloader and someone who bought a house and had an unexpected major repair that the inspector missed and all of a sudden has to come up with $5k fast. And it also ignores that student loan debt can be a very powerful motivator to better their careers, depending on their personality. But if you're able, being there as a safety net or helping to pay for college, or even covering the bill fully, will help them tremendously in life. From a post I made in another thread:

This was specifically about student loans, substitute student loans and college for startup costs for their own business, or a down payment on a house, or moving costs to move to a place with better career opportunities...

And back to our regularly scheduled discussion about what makes different classes.

In reply to RX Reven' :

On that same page, it's a little demoralizing to work for almost half a year and have that money not matter because daily swings are bigger than your total take home during that time.

The hard part for people is going from accumulating to spending.

It would be interesting to chart how close we were to a leisure economy throughout recent history.

This article covers it, but it's fairly old now. It'd be nice to see it updated past 1995. https://eh.net/encyclopedia/hours-of-work-in-u-s-history/

Here's another. https://www.brookings.edu/wp-content/uploads/2020/08/The-Middle-Class-Time-Squeeze_08.18.2020.pdf With a good chart:

Notice that outside of the Great Recession, the amount of hours worked has actually increased for most married couples since the 70's.

RX Reven' said:mtn said:In reality, it looks like a very, very steep quarter-pipe.FYI, the proper statistical term for that type of distribution is "skewed to the right".

Wearymicrobe shared that he's worth a little over 10 million...last time I checked, the top 1% had a net worth of 11.3 million so he's right on the number despite being worth many, many, many times more than the average person.

Call me obsessed but I calculate my net worth, to the penny, at the close of nearly every trading day....literally, if I buy a soda or whatever, I pull a buck fifty out of my net worth. At the end of each year I perform a calculation that I've never seen financial advisors do...I work out the ratio of organic vs inorganic growth to my portfolio. Organic = appreciation of my existing investments and inorganic = sweat effort coming from contributing to my 401K, paying down my mortgage, etc.

Over time, organic makes a greater and greater percent contribution relative to inorganic which I think is an elegant way of tracking progress towards becoming irrelevant...think about it, the goal is to make yourself irrelevant (i.e. current efforts are trivial relative to the gains you're getting from previous efforts).

Simply stated "time to retire" can be defined as the point in time where your efforts don't matter very much anymore.

I'm maxed out on my 401K contributions (including catch up) pay down my mortgage 24K per year (I currently owe 50K to the penny as I calculate carried interest each month to hit an exact number) and buy a little stock here and there. Still, my organic to inorganic ratio averages about 5.8 to 1.

I'll be 57 at the end of June and I think I'm on track to making myself irrelevant.

![]() I'm aware.

I'm aware.

I see you as an inspiration btw. And I'm very jealous of wearymicrobes success.

11.3 net worth number is useless to compare yourself to without age. It's a lot more impressive at 30 than it is at 90. So add 'age' to the list of reasons that an income or net worth figure is useless for deciding your economic class.

RX Reven' said:Simply stated "time to retire" can be defined as the point in time where your efforts don't matter very much anymore.

Agreed.

I find myself working toward something different now. I guess one way to word it would be FU money. While my ideal retirement portfolio would have 2M in it (me, not household), I'm pretty comfortable knowing that even with <1M in it, I can decide to go work at a gym or Lowes or something and as long as my basic expenses are met, I will be fine. My portfolio will still grow significantly with no contributions, and even if I go the early retirement route, 1M/25 = $40k/year is enough to survive.

pheller said:

Notice that outside of the Great Recession, the amount of hours worked has actually increased for most married couples since the 70's.

Looking at the line for "Married couples(total)", the real jump just came in the late 70s through the 80s when women entered the workforce en masse. By the mid 90s, dual income households were the norm, and things have been pretty stable around 3600hrs for the last 25 years or so (with the exception of the drop during the Great Recession). The single earner lines are both fairly flat too, so it seems like hrs worked per employee are pretty consistent over the time of that chart. The only difference is that there are likely to be more workers per household now.

STM317 said:pheller said:

Notice that outside of the Great Recession, the amount of hours worked has actually increased for most married couples since the 70's.

The real jump just came in the late 70s through the 80s when women entered the workforce en masse. By the mid 90s, dual income households were the norm, and things have been pretty stable around 3600hrs for the last 25 years or so (with the exception of the drop during the Great Recession).

I think that is an interesting chart because a big chunk of the US doesn't have the option of changing their hours. I could live quite comfortably on less pay & less hours, but that isn't an option.

Also interesting is that as the average # of hours went up, I bet the "standard of living" shot up as well. The average home size, # meals out, cars per household, boats per household, travel budget, etc. probably all jumped significantly.

a big chunk of the US doesn't have the option of changing their hours. I could live quite comfortably on less pay & less hours, but that isn't an option.

Pretty much any retail place will employ a person part time. Especially in the current environment where they're desperate for bodies. You could negotiate a flexible schedule and (relatively) decent wage pretty easily. The FedEx hub near me was starting people over $20hr 10 years ago when I worked there. You worked about 20-25hrs per week with solid benefits. I'd imagine the $$$ rate has gone up since then. If you want to work fewer hours, and you're comfortable making less money I'd say there are plenty of options.

mazdeuce - Seth said:In reply to RX Reven' :

On that same page, it's a little demoralizing to work for almost half a year and have that money not matter because daily swings are bigger than your total take home during that time.

The hard part for people is going from accumulating to spending.

I totally understand that, a standard 10% market correction would cost me 15 months in in gross salary at this point.

You just have to trust that the universe tends to favor responsible aggression and...

STM317 said:a big chunk of the US doesn't have the option of changing their hours. I could live quite comfortably on less pay & less hours, but that isn't an option.

Pretty much any retail place will employ a person part time. Especially in the current environment where they're desperate for bodies. You could negotiate a flexible schedule and (relatively) decent wage pretty easily. The FedEx hub near me was starting people over $20hr 10 years ago when I worked there. You worked about 20-25hrs per week with solid benefits. I'd imagine the $$$ rate has gone up since then. If you want to work fewer hours, and you're comfortable making less money I'd say there are plenty of options.

In certain brackets yes. What I meant by a 'big chunk' that is many people have white collar jobs where reduced hours are not an option. For example, for those making $100K, working 4 days a week for $80K isn't going to happen.

In reply to mtn :

So...

Middle Class = You inspire people

Upper Class = You make people jealous

Got it ![]()

Don't forget, a lot of wealth comes from the miracle of compound interest.

Most of Warren Buffet's fortune only showed up in the last 20 years or so, thanks to compounding.

If you're just starting out investing, it seems to get nowhere but you have to remember, it's like a snowball rolling down hill.

RX Reven' said:In reply to mtn :

So...

Middle Class = You inspire people

Upper Class = You make people jealous

Got it

Lol - I see what you've done, and it is attainable to me with hard work. I see Wearymicrobe, and I don't see a path to that for myself without a significant amount of luck.

ProDarwin said:STM317 said:a big chunk of the US doesn't have the option of changing their hours. I could live quite comfortably on less pay & less hours, but that isn't an option.

Pretty much any retail place will employ a person part time. Especially in the current environment where they're desperate for bodies. You could negotiate a flexible schedule and (relatively) decent wage pretty easily. The FedEx hub near me was starting people over $20hr 10 years ago when I worked there. You worked about 20-25hrs per week with solid benefits. I'd imagine the $$$ rate has gone up since then. If you want to work fewer hours, and you're comfortable making less money I'd say there are plenty of options.

In certain brackets yes. What I meant by a 'big chunk' that is many people have white collar jobs where reduced hours are not an option. For example, for those making $100K, working 4 days a week for $80K isn't going to happen.

One time when interviewing for a job (they recruited me, I wasn't really looking to move) i asked them this directly. I wanted the 4 days for 20% salary cut.

They rescinded their offer.

Robbie (Forum Supporter) said:ProDarwin said:STM317 said:a big chunk of the US doesn't have the option of changing their hours. I could live quite comfortably on less pay & less hours, but that isn't an option.

Pretty much any retail place will employ a person part time. Especially in the current environment where they're desperate for bodies. You could negotiate a flexible schedule and (relatively) decent wage pretty easily. The FedEx hub near me was starting people over $20hr 10 years ago when I worked there. You worked about 20-25hrs per week with solid benefits. I'd imagine the $$$ rate has gone up since then. If you want to work fewer hours, and you're comfortable making less money I'd say there are plenty of options.

In certain brackets yes. What I meant by a 'big chunk' that is many people have white collar jobs where reduced hours are not an option. For example, for those making $100K, working 4 days a week for $80K isn't going to happen.

One time when interviewing for a job (they recruited me, I wasn't really looking to move) i asked them this directly. I wanted the 4 days for 20% salary cut.

They rescinded their offer.

I've had similar. I was, at the time, on 4x10's and told them I wanted the same, and also that they needed to match my current vacation which would have amounted to 5 more days than they offered.

Nope, they couldn't do either. Ok, not interested. Thanks for calling (I wasn't interested anyway, but figured that it was worth at least interviewing. Didn't get to the offer yet)

ShawnG said:Don't forget, a lot of wealth comes from the miracle of compound interest.

Most of Warren Buffet's fortune only showed up in the last 20 years or so, thanks to compounding.

If you're just starting out investing, it seems to get nowhere but you have to remember, it's like a snowball rolling down hill.

This is where that "a little help from my parents" thing is bigger than most people want to admit. Paying 8% on $100k and earning 8% on 100k is a spread of 16%. Pay for their college and make sure they have a co-signer/down payment on their first house and the difference after 20 years is staggering.

This topic is locked. No further posts are being accepted.