Looking for some retirement advice here guys.

Background - Married, no kids, no real plans for kids. Me: 37 - Wife - 34

Both work professional jobs with regular salaries.

No debt besides house (6.5 years left at $1500/month), wife's student loans (making payments and leaning on loan forgiveness/nonprofit sector employment), and wife's car (2016 Kia Optima, pays around $330/month). No credit card debt at all, use CC daily and pay off monthly. Not looking to buy a new house in the near future, our current place will be our forever home unless something spectacular comes along.

We have minimal mixed finances, her money is hers, my money is mine, we take turns buying groceries, house stuff or big trips come out of a joint slush fund we have ~$12k in give or take. Mainly leftover wedding money, tax returns, refund checks for various things, and a few overpayments based on how our money goes into that account.

Right now we are maxing the 401k contributions and whatever her non-profit similar thing is called, she will get a pension as a state employee in another few months - 5 year minimum.

Need to find something to do with the $30k of cash we have kicking around in various checking and savings accounts, and maybe a way to prevent it from getting so large. Should we start an IRA? I dont have one or know much about it. Right now we have some stuff stuck in CDs but that is only earning around 2.5%.

We both grew up poor so we both have the mindset of "cash is king". My parents pay cash for everything even their house. My family never grew up getting loans, I have only ever had one car loan on my Viper (paid off now) and my house.

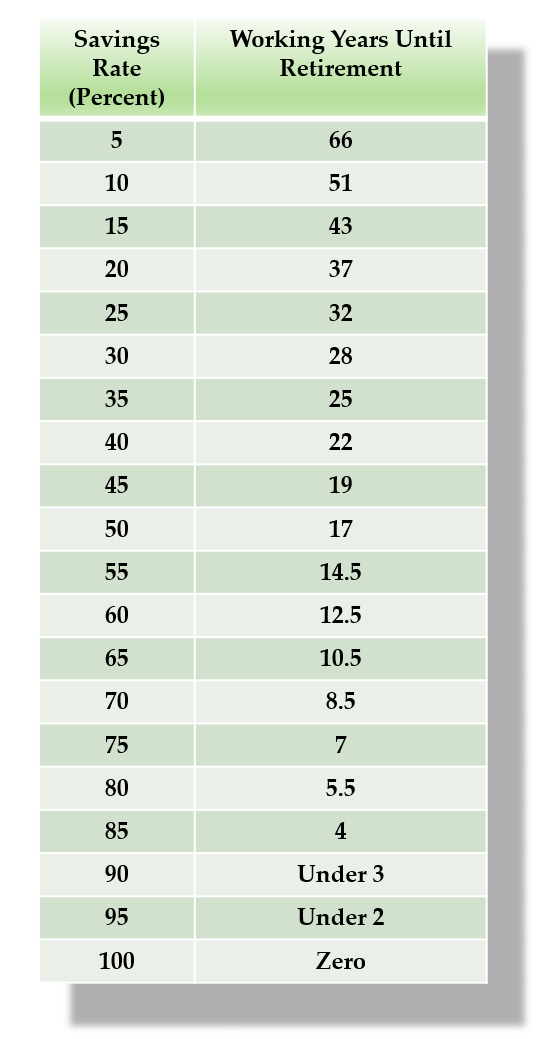

Would really love to have both of us retire in our early 50s, so 15-20 years.

What I need help with is getting over the "cash is good, debt is bad, investments other than liquidity are scary" mindset. Short of going to see an actual financial planner, which may be the right thing to do anyway, where can I start getting resources?